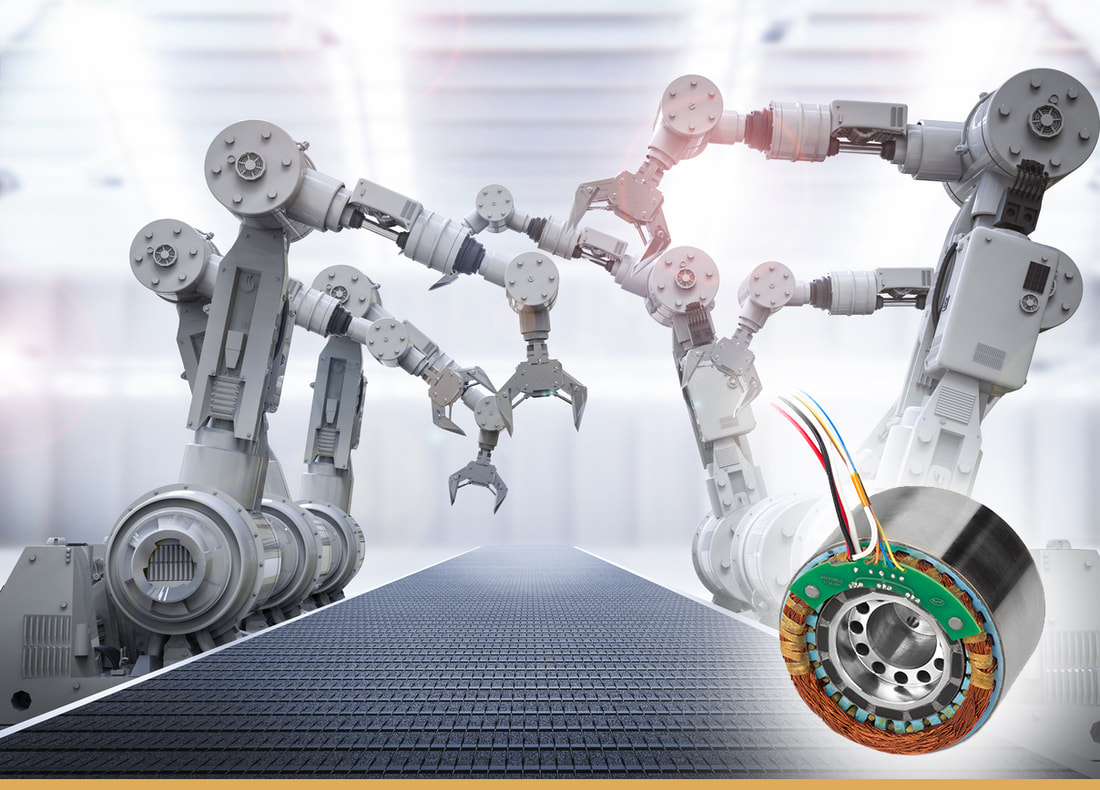

Industrial Robotics Market Industrial robotics include robotic arms, robotic grippers, and robotic tools that are used in various industrial automation processes such as material handling, welding, painting, assembly, packaging and product inspection among others. Industrial robots reduce the dependence on human workforce, improve production efficiency and consistently provide high-quality output to meet the global demand of commercial products and goods. Industrial robotics enable mass production in a cost-effective manner and minimizes wastage of raw materials. Robots have advanced sensors and controls that allow them to perform complex tasks with precision and consistency resulting in reduced production cycle time and less rework.

The global industrial robotics Market is estimated to be valued at US$ 60.91 Mn in 2023 and is expected to exhibit a CAGR of 4.8% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Cost Reduction in Assembly Line Automation Industrial robots provide significant cost savings to manufacturers by automating manual and repetitive assembly line tasks. Robots can work tirelessly in production lines without needing breaks and are not prone to errors caused by human fatigue. This leads to higher production volume, improved quality and reduced costs. Automating manual processes using robots eliminates costs associated with human labor such as wages, benefits, injuries and absenteeism. Robotic arms and tools can work 24/7 and complete tasks faster than humans, resulting in optimized utilization of facility space and resources. Assembly automation with robots minimizes rejects and reworks, significantly cutting down on material wastage. Overall, industrial robotics enable mass customization at lower unit costs by streamlining assembly operations. This presents a major market opportunity for industrial robotics manufacturers to automate manual assembly lines across industries and help customers reduce production costs. Porter’s Analysis Threat of new entrants: The industrial robotics market requires significant capital investments for R&D, production facilities, skilled workforce etc. Established players enjoy economies of scale. These factors make the threat of new entrants moderate. Bargaining power of buyers: The bargaining power of buyers is moderate as the industrial robotics technology is still nascent with limited alternatives. However, large factories have higher bargaining power. Bargaining power of suppliers: Key components like actuators, gears etc. are highly specialized with few global suppliers. This gives them moderate bargaining power over manufacturers. Threat of new substitutes: While additive manufacturing and other future technologies offer substitutions, they are yet to match the capabilities of industrial robotics. Substitution threat is low at present. Competitive rivalry: The industrial robotics market is highly consolidated with major global players. Intense competition keeps pricing pressure and forces players to invest in new technologies. SWOT Analysis Strengths: Growing automation demand from factories, cost savings compared to human labor, ability to perform repetitive & dangerous tasks accurately. Weaknesses: High initial installation costs, need for specialized engineering skills, limited flexibility for small batch production. Opportunities: Scope for collaborative robots, machine learning integration, remote monitoring & maintenance, expansion in SMEs and new applications. Threats: Trade barriers affecting global supply chains, economic slowdowns reducing factory investments, slow consumer adoption of robotic applications. Key Takeaways The Global Industrial Robotics Market Growth is expected to witness high at a CAGR of 4.8% during the forecast period of 2023 to 2030. Rapid factory automation driven by rising labor costs and the need for 24/7 operations will propel demand. Asia Pacific dominates currently due to massive electronics and automobile manufacturing in China, Japan, South Korea. Countries like China, Japan and South Korea are investing heavily in advanced robotics R&D and witness highest installation rates. Europe and North America are other major regional markets driven by strong automotive, food & beverage sectors. China alone accounts for over 30% of installations worldwide attributed to the massive manufacturing sector. Japan and South Korea also have a well-established robotics industry. Key players operating in the industrial robotics market are Asahi Glass Co. Ltd. (AGC), Corning Incorporated, SCHOTT AG, Incom Inc., Hamamatsu Photonics K.K., Nippon Electric Glass Co., Ltd. (NEG), II-VI Incorporated, Hamamatsu Corporation, Saint-Gobain S.A., Asahi Kasei Corporation, Leoni AG, TDK Corporation, Mitsubishi Chemical Corporation, Furukawa Electric Co., Ltd., GS Plastic Optics. These players are focusing on developing innovative collaborative robots catering to SMEs and new application areas like logistics, healthcare, and more. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/industrial-robotics-market-share-size-and-growth-share-trends-analysis-demand-forecast/

0 Comments

Leave a Reply. |

AuthorWrite something about yourself. No need to be fancy, just an overview. ArchivesCategories |

RSS Feed

RSS Feed